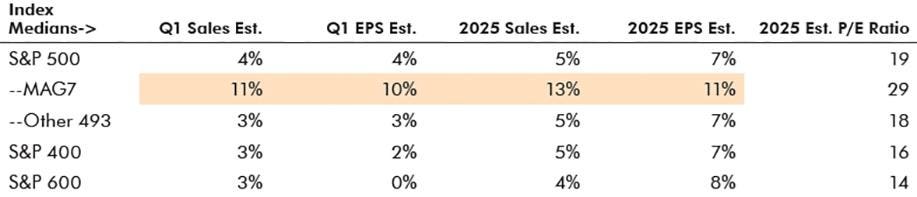

The U.S. equity market has been difficult so far in 2025. After the sharp drop this Thursday, the S&P 500 was down nearly 8% YTD and 12% off all-time highs due to fears on stagflation and worries over the Trump Administration’s newest tariff policies. Interestingly, this is against a backdrop of expected sales and earnings growth for the rest of the year in U.S. stocks. Figure 1 below shows the consensus Q1 and 2025 estimates for large-cap, mid-cap, and small-cap stocks. All are expected to record good earnings growth for the full year of +7-8%. For the Q1 2025, small-cap stocks are expected to show no earnings growth but mid- and large-caps are expected to report +5% gains. Similarly, stocks are expected to have sales growth for both the first quarter at +3-4% and the full year at +4+5%. Despite recent softer economic data and fears of restrictive economic policy, investors continue to have a relatively sanguine outlook for U.S. equity fundamentals.

Figure 1: Median Growth Estimates for S&P Baskets

Figure 2 combines market cap ranges and consensus estimates by sector for Q1 and 2025. Notably, five of 11 William O’Neil sectors are forecast to see a decline in earnings in Q1 2025: Basic Materials, Consumer Cyclical, Consumer Staple, Energy, and Retail. Despite this, all 11 sectors are forecast to have positive sales and earnings growth for the full year of 2025. We are skeptical that this will actually occur. Technology and Utilities are projected to have the strongest full-year sales growth at +7% with Technology and Transportation forecast to have the best earnings growth at +11% and +15%, respectively.

Figure 2: Median Growth Estimates for O’Neil Sectors

One reason for our skepticism is that sales and earnings estimates have been falling rapidly entering earnings season as seen in Figure 3 from Bloomberg below. The rate at which estimates have declined makes us cautious entering next week when earnings season begins. While the U.S. stock market is oversold, we believe any bounce is likely to be short lived until estimates for sales and earnings are reset lower.

Figure 3: Bloomberg Guidance Momentum Score, 2022–2025

Figures 4 and 5 show revisions by market cap ranges and by sector. In terms of market cap, small stocks represented by the S&P 600 have had the worst estimate revisions. This is troubling as rapidly decreasing small-cap estimates are usually a harbinger of weaker domestic growth. Interestingly, revisions for the Mag 7 have been in-line with revisions for large-cap stocks overall. Because of this, the Mag 7 may lose some of their quality premium versus the S&P 500.

Figure 4: Index Estimate Revisions over Past 60 Days

In terms of sectors, much like small-caps, the more cyclical areas of the market such as Transportation, Retail, Consumer Cyclical, and Basic Materials have seen the worst negative earnings revisions. Again, we believe this is a precursor to slower U.S. economic growth and future revisions downward for full-year 2025 estimates.

Figure 5: Sector Estimate Revisions Over the Past 60 Days

Technically, the S&P 500 as well as other U.S. stock benchmarks, has experienced a great deal of damage. Below in Figure 6 is data for the S&P 500 relating to breaks of the 200-DMA, since 1990. We used a minimum of three days below the 200-DMA as a starting point, and counted a consecutive period below as long as there were not more than three days back above the 200-DMA. The bracketed periods are part of a longer period where the index traded back and forth above/below the 200-DMA. Our worry is that, given the depth now below the 200-DMA (more than the average/median of below periods), the recent pullback represents a trend change and the start of a new bear market. Avoiding the prolonged downtrend is still possible and there are several of these examples in the past to point to. However, at this point it is unclear how the current action will resolve itself.

Figure 6: Instances of S&P 500 Trading Below 200-DMA after Prior Uptrend

Presently, William O’Neil + Co. has the market rated Downtrend. As it once again undercut the previous low, we need to see four days off the lows in order to open the window for a follow-through day (FTD) (>1.7% price move on S&P 500 or Nasdaq on volume higher than prior day). Here is a refresh of the data we sent a few weeks ago on FTDs from below the 200-DMA on the S&P 500. While we are hopeful the market can rally before we are deep into earnings season, we remain very cautious as we believe many individual stocks will see further price pullbacks when they offer revised Q2 and full year guidance on their upcoming conference calls. As a result, it is possible that the first FTD in this cycle will not be successful.

On the S&P 500, there have been 35 corrections of at least 9% and to below the 200-DMA since 1970. Of these: • Scenario One-Bull Case #1 – 19 had a first FTD which resulted in the continuation of the bull market and eventual new highs.

- Scenario Two-Bull Case #2 – Eight had a first failed FTD, but then a second which resulted in the continuation of the bull market and eventual new highs.

- Scenario Three-Bear Case #3 – Eight resulted in an eventual bear market. Of these, six had at least four failed FTDs. The years 1987 and 2020 were exceptions where the first FTD was never undercut.

For now, we’ll just focus on the scenario one, as a FTD now would be the first one since the break of the 200-DMA four weeks ago.

Figure 7: Scenario 1-Bull Case #1-19 Bull Market Corrections in which the First Follow-Through Day Led to New Highs

The keys in this scenario include:

- No undercut of lows established prior to the FTD.

- Strong progress made after the FTD, usually within 4–8 weeks. Conversely, at most minor losses from the FTD close.

See the S&P 500 chart below. While we had hoped for a quick retake of the 200-DMA (40-WMA), that has not happened. This leaves 2018–2019 as the more relevant scenario in recent history (one failed FTD before a second successful one). Post FTDs, some distribution is normal. However, immediate losses after the FTD or more than a few distribution days tend to dramatically lower the chances of success. For the first two scenarios, here are the historical distribution days (DDays) within the first four weeks.

Kenley Scott, Director, Global Sector Strategist at William O’Neil + Company, an affiliate of O’Neil Global Advisors, made significant contributions to the data compilation, analysis, and writing for this article.

The William O’Neil + Co. Research Analysts made significant contributions to the data compilation, analysis, and writing for this article.

Disclaimer

No part of the authors’ compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed herein. William O’Neil + Co., its affiliates, and/or their respective officers, directors, or employees may have interests, or long or short positions, and may at any time make purchases or sales as a principal or agent of the securities referred to herein.

William O’Neil + Co. Incorporated is an SEC Registered Investment Adviser. Employees of William O’Neil + Company and its affiliates may now or in the future have positions in securities mentioned in this communication. Our content should not be relied upon as the sole factor in determining whether to buy, sell, or hold a stock. For important information about reports, our business, and legal notices please go to www.williamoneil.com/legal.

©2025, William O’Neil + Company, Inc. All Rights Reserved.

Read the full article here